%22 fill-rule=%22nonzero%22%3E%3Cpath d=%22M15.754367 31.4866226c-4.2011645.0-8.13699236-1.636243-11.14414171-4.5991696-6.14696705-6.146967-6.14696705-16.0970936.0-22.24406062C7.57315186 1.68046581 11.5532025.0442227846 15.754367.0442227846S23.8913594 1.68046581 26.8985087 4.64339238L21.6359973 9.90590374c-2.2995848-2.2995848-5.7489619-3.09559492-9.0656708-1.85735695C8.28071641 9.99434931 6.37913667 14.5492961 8.05960249 18.9715746c1.45935189 3.2282632 4.46650121 5.129843 7.73898731 5.129843 2.2111392.0 4.2896101-.8844557 5.8816303-2.4322532l5.2625114 5.2625114c-3.0071494 2.9187038-6.9872 4.5549468-11.1883645 4.5549468z%22 id=%22%E8%B7%AF%E5%BE%84%22 fill=%22%23001f60%22/%3E%3Cg id=%22%E7%BC%96%E7%BB%84%22 transform=%22translate(31.099673, 0.663342)%22%3E%3Cpolygon id=%22%E8%B7%AF%E5%BE%84%22 fill=%22%23001f60%22 points=%220 14.5050733 0 30.2041619 7.42942781 30.2041619 7.42942781 7.11986831%22/%3E%3Crect id=%22%E7%9F%A9%E5%BD%A2%22 fill=%22%2300bbb4%22 x=%220%22 y=%22-125688713e-22%22 width=%227.42942781%22 height=%227.11986831%22/%3E%3C/g%3E%3Cpath d=%22M99.6449893 19.0600201C98.1414146 13.6648404 92.525121 12.6919392 87.9701742 11.895929 87.5279463 11.8074835 87.0414957 11.7190379 86.5992679 11.6305923 83.5921185 11.0556961 83.3267818 10.878805 82.884554 10.6134683 82.0885438 10.0827949 82.0885438 9.06567084 82.4423261 8.49077464 83.0614451 7.47365059 84.6976881 6.89875439 86.6434907 6.89875439c4.0242733.0 5.2625113 1.7246886 5.4394025 2.74181264H99.7334349c0-2.43225315-1.4151291-4.95295187-3.75893670000001-6.76608603C94.2498096 1.54779746 91.2426602.0 86.5992679.0 81.4252021.0 78.4622755 1.94580252 76.914478 3.58204555 75.2340122 5.35095693 74.3495565 7.65054173 74.4380021 9.90590374 74.7033388 16.1855391 80.3638552 18.0428961 85.2725843 18.9273518 85.759035 19.0157974 86.2454856 19.1042429 86.7319362 19.1926885 87.9259514 19.4138024 89.4737489 19.6349163 90.7562096 20.0329214 91.5964425 20.2982581 92.4366754 21.0500455 92.0828932 22.2440606c-.2653368.8402329-1.6804659 1.9458026-4.2011646 2.1669165C85.2283615 24.632091 83.1056679 23.9687492 82.1327666 22.8631796 81.4694249 22.1556151 81.3809793 21.2711594 81.3809793 20.8289315H73.9515515C73.9515515 23.5707442 75.1013439 26.0914429 77.135592 27.9930226c2.3880303 2.2111393 5.8816303 3.4051544 9.6847898 3.4051544C87.3510552 31.398177 87.8817286 31.3539543 88.412402 31.3097315 92.8346805 30.9117264 96.3725033 29.142815 98.3183058 26.3567796 99.9545488 24.2783087 100.396777 21.6691644 99.6449893 19.0600201z%22 id=%22%E8%B7%AF%E5%BE%84%22 fill=%22%23001f60%22/%3E%3Cpath d=%22M71.6519667 30.8675036 63.7360882 20.2098125C67.9372528 19.0157974 70.9886249 15.2126379 70.9886249 10.6134683 70.9886249 5.12984301 66.5221237.663341768 61.0384984.663341768H44.8529592V30.8675036H52.282387V20.5635948h3.2282633l7.606319 10.3039088h8.5349974zM52.2381643 7.82743287h8.3581062c1.59202029999999.0 2.874481 1.28246075 2.874481 2.87448103.0 1.5920202-1.2824607 2.874481-2.874481 2.874481H52.2381643V7.82743287z%22 id=%22%E5%BD%A2%E7%8A%B6%22 fill=%22%23001f60%22/%3E%3C/g%3E%3C/g%3E%3C/svg%3E)

%22%3E%3Cg id=%22%E7%BC%96%E7%BB%84-34%22 transform=%22translate(1654.000000, 46.000000)%22%3E%3Cg id=%22%E7%9F%A9%E5%BD%A2%22 opacity=%22.01%22%3E%3Cuse fill=%22%23fff%22 xlink:href=%22%23path-1%22/%3E%3Cuse fill=%22%23f2f3f7%22 xlink:href=%22%23path-1%22/%3E%3C/g%3E%3Cg id=%22sousuo%22 transform=%22translate(6.000000, 6.000000)%22%3E%3Cmask id=%22mask-3%22 fill=%22%23fff%22%3E%3Cuse xlink:href=%22%23path-2%22/%3E%3C/mask%3E%3Cg id=%22Clip-2%22/%3E%3Cpath d=%22M11.6489827.0271704545c6.433526.0 11.6491213 5.1088636355 11.6491213 11.4108750455.0 2.9073068-1.110104 5.5606704-2.9376763 7.5756477C20.393341 19.0389886 20.424763 19.0662955 20.4543121 19.0953068l3.24437 3.1817727C24.099711 22.6703523 24.1004046 23.3084659 23.7004509 23.7025227L23.6986821 23.7042614C23.2966127 24.0985568 22.6454913 24.0985568 22.243422 23.7042614l-3.2445434-3.1817728C18.9553873 20.4797386 18.915815 20.433375 18.8807514 20.3838409L18.8809942 20.3841136c-1.986763 1.5431591-4.4995838 2.4646705-7.2320115 2.4646705C5.21545665 22.8487841.0 17.7400568.0 11.4380455.0 5.13603409 5.21545665.0271704545 11.6489827.0271704545zm0 2.0661136355c-5.26855495.0-9.53975727 4.18384091-9.53975727 9.34476141.0 5.1609204 4.27120232 9.344625 9.53975727 9.344625 5.2686936.0 9.5397225-4.1837046 9.5397225-9.344625.0-5.1609205-4.2710289-9.34476141-9.5397225-9.34476141z%22 id=%22Fill-1%22 fill=%22%23424242%22 mask=%22url(%23mask-3)%22/%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E)

%22%3E%3Cg id=%22%E7%BC%96%E7%BB%84-8%22 transform=%22translate(1165.000000, 90.000000)%22%3E%3Cg id=%22%E7%BC%96%E7%BB%84-5%22 transform=%22translate(30.000000, 35.000000)%22%3E%3Cg id=%22%E7%BC%96%E7%BB%84-6%22 transform=%22translate(413.000000, 3.000000)%22%3E%3Cg id=%22sousuo%22 transform=%22translate(12.000000, 12.000000)%22%3E%3Cmask id=%22mask-2%22 fill=%22%23fff%22%3E%3Cuse xlink:href=%22%23path-1%22/%3E%3C/mask%3E%3Cg id=%22Clip-2%22/%3E%3Cpath d=%22M14.6489827 3.02717045c6.433526.0 11.6491213 5.10886364 11.6491213 11.41087505.0 2.9073068-1.110104 5.5606704-2.9376763 7.5756477C23.393341 22.0389886 23.424763 22.0662955 23.4543121 22.0953068l3.24437 3.1817727C27.099711 25.6703523 27.1004046 26.3084659 26.7004509 26.7025227L26.6986821 26.7042614C26.2966127 27.0985568 25.6454913 27.0985568 25.243422 26.7042614l-3.2445434-3.1817728C21.9553873 23.4797386 21.915815 23.433375 21.8807514 23.3838409L21.8809942 23.3841136c-1.986763 1.5431591-4.4995838 2.4646705-7.2320115 2.4646705C8.21545665 25.8487841 3 20.7400568 3 14.4380455 3 8.13603409 8.21545665 3.02717045 14.6489827 3.02717045zm0 2.06611364c-5.26855495.0-9.53975727 4.18384091-9.53975727 9.34476141.0 5.1609204 4.27120232 9.344625 9.53975727 9.344625 5.2686936.0 9.5397225-4.1837046 9.5397225-9.344625.0-5.1609205-4.2710289-9.34476141-9.5397225-9.34476141z%22 id=%22Fill-1%22 stroke=%22%23f2fbff%22 fill=%22%23f5f5f5%22 mask=%22url(%23mask-2)%22/%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E)

%22%3E%3Cg id=%22%E7%BC%96%E7%BB%84-19%22 transform=%22translate(515.000000, 180.000000)%22%3E%3Crect id=%22%E7%9F%A9%E5%BD%A2%22 fill=%22%23fff%22 opacity=%22.2%22 x=%220%22 y=%220%22 width=%2280%22 height=%2280%22 rx=%2240%22/%3E%3Cg id=%22sousuo%22 opacity=%22.7%22 transform=%22translate(21.000000, 21.000000)%22%3E%3Cmask id=%22mask-2%22 fill=%22%23fff%22%3E%3Cuse xlink:href=%22%23path-1%22/%3E%3C/mask%3E%3Cg id=%22Clip-2%22/%3E%3Cpath d=%22M18.4442225.0430198864c10.1864162.0 18.4444422 8.0890340936 18.4444422 18.0672187136.0 4.6032358-1.7576647 8.8043949-4.6513208 11.9947756C32.2894566 30.1450653 32.3392081 30.1883011 32.3859942 30.2342358l5.1369191 5.0378068C38.1578757 35.8947244 38.158974 36.905071 37.5257139 37.5289943L37.5229133 37.5317472C36.8863035 38.1560483 35.8553613 38.1560483 35.2187514 37.5317472l-5.1371936-5.0378069C30.0126965 32.4262528 29.9500405 32.3528437 29.8945231 32.2744148L29.8949075 32.2748466C26.7491994 34.7181818 22.7705665 36.1772415 18.4442225 36.1772415 8.25780636 36.1772415.0 28.0884233.0 18.1102386.0 8.13205398 8.25780636.0430198864 18.4442225.0430198864zm0 3.2713465936c-8.3418786.0-15.10461556 6.62441477-15.10461556 14.79587212.0 8.1714574 6.76273696 14.7956563 15.10461556 14.7956563 8.3420983.0 15.1045607-6.6241989 15.1045607-14.7956563.0-8.17145735-6.7624624-14.79587212-15.1045607-14.79587212z%22 id=%22Fill-1%22 fill=%22%23000%22 mask=%22url(%23mask-2)%22/%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E)

%22%3E%3Cg id=%22%E7%BC%96%E7%BB%84-11%22 transform=%22translate(625.000000, 180.000000)%22%3E%3Cg id=%22%E7%9F%A9%E5%BD%A2%22 opacity=%22.1%22%3E%3Cuse fill=%22%23fff%22 xlink:href=%22%23path-1%22/%3E%3Cuse fill=%22%23000%22 xlink:href=%22%23path-1%22/%3E%3C/g%3E%3Cg id=%22%E5%BD%A2%E7%8A%B6%E7%BB%93%E5%90%88-2%22 opacity=%22.9%22 transform=%22translate(23.000000, 23.000000)%22 fill=%22%23fff%22%3E%3Cpath d=%22M3.41421356.585786438 16.849 14.02 30.2842712.585786438C31.024212-.154154326 32.1996962-.193098576 32.9854836.468953686L33.1126984.585786438C33.893747 1.36683502 33.893747 2.63316498 33.1126984 3.41421356L19.677 16.849 33.1126984 30.2842712C33.893747 31.0653198 33.893747 32.3316498 33.1126984 33.1126984s-2.0473786.781048599999998-2.8284272.0L16.849 19.677 3.41421356 33.1126984C2.6742728 33.8526391 1.49878864 33.8915834.713001205 33.2295311L.585786438 33.1126984c-.781048584-.781048599999998-.781048584-2.0473786.0-2.8284272L14.02 16.849.585786438 3.41421356c-.781048584-.78104858-.781048584-2.04737854.0-2.828427122.781048582-.781048584 2.047378542-.781048584 2.828427122.0z%22 id=%22%E5%BD%A2%E7%8A%B6%E7%BB%93%E5%90%88%22/%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E)

%22 fill=%22%23fff%22 stroke=%22%23fff%22 stroke-width=%22.5%22%3E%3Cg id=%22%E7%BC%96%E7%BB%84-5%22 transform=%22translate(45.000000, 1550.000000)%22%3E%3Cg id=%22diqiu-(1)%22 transform=%22translate(5.002008, 10.003347)%22%3E%3Cpath d=%22M11.9962845.0c6.6265774.0 11.9982929 5.37184937 11.9982929 11.9982929.0 6.6265774-5.3717155 11.9983263-11.9982929 11.9983263-6.6264435.0-11.9982928682-5.3717489-11.9982928682-11.9983263C-.0020083682 5.37184937 5.369841.0 11.9962845.0zM5.77114644 3.6685523 5.72669456 3.70162343C3.21844351 5.60016736 1.59775732 8.6099749 1.59775732 11.9982929 1.59775732 12.2123515 1.60428452 12.4248368 1.61697071 12.6355816L1.61723849 12.6354477C3.80421757 11.9799833 5.42148954 12.1131046 6.48046862 13.1906276 7.01616736 13.7358661 7.31939749 14.337205 7.41991632 15.048L7.42530544 15.0886695C7.44920502 15.2762845 7.45770711 15.4316318 7.4620251 15.7256904L7.46440167 15.9032301C7.47353975 16.3908285 7.51929707 16.5114979 7.75414226 16.8110795 7.93077824 17.0341423 8.13174895 17.228954 8.38711297 17.4240335 8.51106276 17.5184268 8.638159 17.6082678 8.76853556 17.6936569L8.82343096 17.7293389 9.27899582 18.0308619 9.30734728 18.0500753C10.342795 18.7493556 10.8550628 19.4148954 11.0353808 20.4309623 11.1534728 21.098477 11.1357992 21.7420251 10.9824268 22.3480837 11.3193975 22.3806192 11.6577741 22.396854 11.9962845 22.396854c5.7429624.0 10.3985272-4.6555988 10.3985272-10.3985611C22.3948117 10.5751967 22.1089874 9.21874477 21.5914644 7.98353138 21.6105774 8.15417573 21.6199833 8.32582427 21.6197155 8.49750628c0 1.45529707-1.1666946 3.77549792-2.8755147 6.02865272C18.6813054 14.6093054 18.6225941 14.6992803 18.564954 14.801272L18.545205 14.8366862 18.5172218 14.8903096C18.4484351 15.0243347 18.3877824 15.16241 18.3353305 15.3037322L18.3107615 15.3716151C18.2834142 15.4470628 18.2570042 15.5227448 18.2315314 15.5988619L18.2066611 15.6740418 18.0977406 16.011113C17.6023431 17.5066778 16.8482678 18.2018745 15.4544603 18.2018745c-.8604854.0-1.4555649-.398125499999999-1.7929038-1.2191465L13.6472971 16.9475816c-.218477-.5481172-.3466109-1.2688536-.5146444-2.7258243L13.105205 13.980251 13.0008703 13.0474644C12.9553808 12.6472301 12.9245188 12.390159 12.8920837 12.1486862L12.86959 11.9809205C12.6048201 10.0421088 12.0975063 7.91096234 11.7792469 7.28411715L11.7695732 7.26530544C11.6725356 7.08066946 11.3546778 6.95320502 10.1593305 6.78269456L10.1228452 6.77760669 10.0539582 6.76830126 9.92046862 6.74935565c-1.3836318-.19979916-1.9576569-.36964017-2.60736402-.81158159C6.50035146 5.38440167 5.98192469 4.6099749 5.77114644 3.6685523zM1.88448536 14.2269791 1.84030126 14.2411046c.84060251 3.8238996 3.78570711 6.8589121 7.55936401 7.8289875C9.52609205 21.6528536 9.54687866 21.200569 9.46021757 20.7099916 9.36646025 20.1814895 9.12508787 19.8620586 8.44033473 19.3950126L8.36619247 19.3450711l-.41579916-.2747113L7.93104603 19.057272 7.8894728 19.0301925C7.74460251 18.9352971 7.60284519 18.8357824 7.46426778 18.7318159L7.41770711 18.6966695C7.05787448 18.4216904 6.76133891 18.1344268 6.49760669 17.8011381 6.01369038 17.1842343 5.87494561 16.7318159 5.86356485 15.8464937L5.86189121 15.7073808C5.85807531 15.4845858 5.8518159 15.3888536 5.83534728 15.2676485 5.78393305 14.9048033 5.63856067 14.6163682 5.33938075 14.3119665 4.76579079 13.7281674 3.65161506 13.6633305 1.88448536 14.2269791zM11.9962845 1.59976569c-1.7042343.0-3.31263596.41004184-4.73221755 1.13676987C7.28328033 3.57245188 7.58754812 4.177841 8.18681172 4.59702092L8.21308787 4.61506276C8.61723849 4.89004184 9.0049205 5.00287866 10.1939749 5.17245188L10.2717992 5.18346444 10.3410879 5.1927364 10.4310628 5.20555649c.768535500000001.11126359 1.2664435.22031799 1.6584435.37576569C12.6001004 5.78373222 12.9554812 6.08291213 13.1851046 6.52c.431999999999999.81877824.989523 3.15755649 1.2774561 5.3032301L14.4914477 12.0402678C14.508318 12.169205 14.5251883 12.3062427 14.5442678 12.4675816L14.5904268 12.8680837 14.7099582 13.9339582c.1594979 1.3988284.276150599999999 2.063297.4311966 2.4406694L15.1582929 16.4159331C15.2323013 16.5917992 15.2551967 16.6017406 15.4406025 16.6021088H15.4544603c.5962175.0.813288699999999-.1828954 1.095297-1.0066611L16.5773724 15.5136067 16.6850879 15.1801841C16.7140084 15.0912803 16.7440669 15.0027448 16.7751967 14.9146109L16.8273473 14.7691046C16.9062092 14.5536067 16.9987615 14.343364 17.1043013 14.1397824L17.140251 14.0717992C17.241205 13.8872971 17.3485523 13.7193975 17.468954 13.5601339c1.5115314-1.9929372 2.5509958-4.06011716 2.5509958-5.06262762C20.0199498 8.06172385 19.9319498 7.6667113 19.6852218 7.00103766L19.5777406 6.71169874C19.4670126 6.41030962 19.4051548 6.22948954 19.3644854 6.088 19.2829121 5.8030795 19.263431 5.59022594 19.3395146 5.34674477 19.391431 5.17874477 19.4713305 5.02065272 19.5755314 4.87906276c-1.8967029-2.0185774-4.5907615-3.27929707-7.5792469-3.27929707z%22 id=%22Fill-1%22/%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E)

For the past few years, China has surpassed Japan and become the world’s 2nd largest market in the total consumption of cosmetics products just after the US. Moreover, L2inc, a business intelligence firm predicts that China will become the largest market of cosmetics products in 2020. Meanwhile, with the quality of consumers’ lives improving, mid-to-high end cosmetics are becoming increasingly popular.

As one of the largest cosmetics markets in the world, new domestic brands keep emerging and piles of international brands contends to swarm into the China market. In order to ensure the quality of products and protect the legitimate rights and interests of consumers, CFDA puts its largest efforts ever in the supervision of the cosmetics industry.

Given all this, combined with the market’s latest development and statistical data upon supervision, CIRS comes with an intuitive and comprehensive analysis of the development of cosmetics industry.

1. Market Scale and Growing Trends

1.1 Overall Industry Continues to Grow

From 2013 to 2016, the total volumes of retail sales of cosmetics continued to increase, with ¥162.5 billion, ¥182.5 billion, ¥204.9 billion and ¥222.2 billion respectively.

By analyzing the moving trend of the year-on-year growth rate of the country’s cosmetics retail sales from January to December 2016, it can be concluded that although there were a few unfulfilling growth rates for certain months, the overall annual sales volume kept increasing. The bottom point of only 4% year-on-year growth rate in 2016 occurred in October. However, with the resumption of the growing rate in the coming months, the retail sales reached ¥22.7 billion in December with the year-on-year growth rate of 11.0%. Consumers’ interests in purchasing are greatly influenced by sales promotions in stores, online platforms and by brand owner companies. Their promotional events in certain periods lead to the unstable monthly growing rates.

According to the Related Analysis of the National Economy published by National Bureau of Statistics in April 2017, the total retail sales from January to April 2017 is ¥78.5 billion with a year-on-year growth rate of 9.4%, higher than the annual growth rate of 8.44% in 2016.

Table 1, Moving Trend of Growth Rate of Cosmetics Retail Sales, January to December, 2016.

Data Source: National Bureau of Statistics; Analyzed by CIRS.

|

Month |

1-2 |

3 |

4 |

5 |

6 |

7 |

8 |

9 |

10 |

11 |

12 |

|

Year-on-Year Growth Rate |

11.4% |

9.2% |

7.6% |

5.9% |

7.9% |

9.0% |

5.8% |

7.7% |

4.0% |

8.1% |

11.0% |

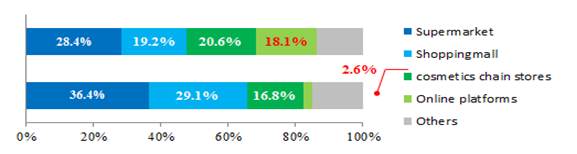

1.2 Revolutionary Change on Sales Channels

The major sales channels for cosmetics are supermarkets, department stores, cosmetics chain stores and online platforms. Cosmetics sales through supermarkets and department stores are still in the dominant position in recent years, however, the scales of the market through chain stores and online platforms are becoming increasingly larger.

Figure 1, Comparison between Different Sales Channels for Cosmetics in 2010 and 2015.

Data Source: China Industrial Information Network; Analyzed by CIRS.

In 2016, the growth rates of cosmetics sales through department stores (skin care and make-ups) and supermarkets (daily care products) are -0.9% and -0.6% respectively. However, the growth rate through cosmetics chain stores (daily care products) has a clear increase of 9.2%, and for online platforms the increase was dramatic of 40%.

Online trading has incomparable geographical and spatial advantages that traditional retail can hardly possess, plus the fact that young buyers are praising highly on online-purchasing these days, the dramatic increase in cosmetic sales through online platforms has then automatically emerged. Cross border e-commerce platforms which developed rapidly due to the low price barrier, have also contributed greatly to the online trading market. From the regional distribution of cosmetics online purchasing, 77% is contributed by the mid-class population in top and 2nd tier cities.

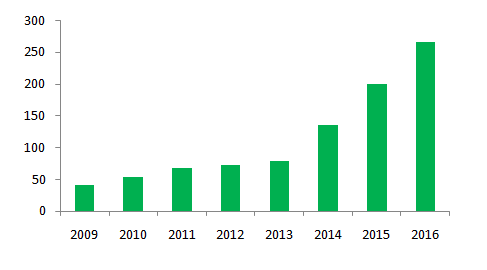

1.3 Increase Market Scale of Import Products vs Slight Decrease for Domestic Products

As one of the largest cosmetics consuming countries with extremely large population base, more and more foreign companies start getting their products into the China market. Furthermore, the cut in cosmetics import tariff has also favored their needs to import products to China. The increasing number of import products increase choices of consumers. Mid-to-high end cosmetics products are highly pursued by the younger generation, which further stimulates the market for import products.

Figure 2, Amount of cosmetics imports (by 100 million RMB) from 2009 to 2016

Data source: Foresight Industry Research Institute; Analyzed by CIRS.

Compared to the rapid growth of the import market, the development on domestic market are experiencing a declining tendency, as popular foreign brands keep swarming into China and the fact that domestic products are trapped into traditional sales channels. Several domestic cosmetics giants started to face downward pressure on profit. In addition, most domestic small and medium-sized brand companies are lack of independent R&D ability and unclear market positioning, which have greatly influenced the quality of domestic products.

1.4 Rapid Growth for the Baby Care Market

More than 15 million infants are born in China annually in recent years, and hundreds of billions are spent on baby care products each year. Data shows that the market volume for 0-3 year old baby care products has reached ¥7 billion in 2016, and the figure is predicted to be more than ¥15 billion in 2020, with the CAGR of 20%.

Table 2, The market volume of 0-3 year old baby care products from 2015 to 2021

Data source: Mintel; Analyzed by CIRS.

|

Year |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

|

Market Volume (by 100 Million) |

55 |

59 |

70 |

88 |

109 |

131 |

154 |

2. Industry Supervision

2.1 Supervision on Cosmetics Manufacturing

On 15th December 2015, CFDA issued the Work Specifications on Cosmetics Production Permit and Checking Points on Cosmetics Production Permit. The ‘Checking Points’ provides specific requirements on different aspects including on institutions and workers, quality control, factory and facilities, equipment, materials and products, production control, verification, product distribution, customer complaints, adverse effects and product recall. It is said to be the China Cosmetics Good Manufacturing Practices.

From 1st January 2016, any newly established cosmetics manufacturer can apply to the local provincial FDA for production license. Provincial FDA shall audit the manufacturing company according to the ‘Specifications’ and issue the Production License to qualified manufacturers.

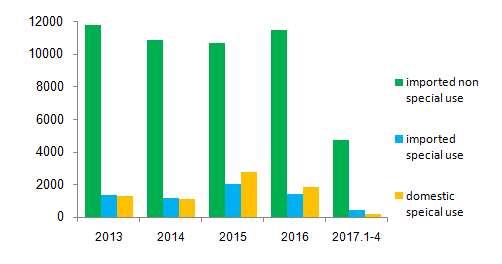

2.2 Current Status of Cosmetics Administrative Approval

In 2016, there are over 11,000 import non-special use cosmetics products, 1,400 import special use products, 1,800 domestic special use products approved by CFDA and 303,700 domestic non-special use cosmetics products recorded at provincial FDAs. Compared with imported non special use cosmetics, less special use cosmetics are approved by CFDA as result of more registration requirements for functional ingredients.

At the end of 2013, CFDA issued the Notice on Adjusting the Management of Cosmetics Registration and Record-Keeping. The notice stated that whitening products are in the scope of anti-freckle products. The transition time for this adjustment was valid until 30th June 2015. Therefore a significant increase of the applications of special use cosmetics products has emerged since 2015.

Figure 3, Data summary of approval import non special use and special use cosmetics from 2013 to 2017

Data Source: CFDA Official Website; Analyzed by CIRS.

From January to April 2017, CFDA has approved about 5,000 import cosmetics and 160 domestic special use products. 31st December 2016 is the expiration date of changing or renewing production license. Moreover, the Technical Safety Standards for Cosmetics (Please click here for more information about the Technical Safety Standards for Cosmetics) was implemented at the same time in December. Most domestic manufacturing companies are experiencing transitional period, causing the significant decrease in the number of applications.

2.3 Market Supervision

In 2016, CFDA has carried out several tests for randomly selected commercially available cosmetics and has paid significant higher attention on sun-blocks, masks and products for anti-acne and anti-freckle compared to other products. In the first quarter of 2017, local FDAs have drawn up the work points on the post-market supervision of cosmetics in many cities and regions. The points are all aimed at monitoring the quality of products, and hence protect the legitimate rights and interests of consumers.

On 1st March 2017, the pilot record-keeping system in Shanghai Pudong New Area has implemented for import non-special use cosmetics. The new system has altered the way of product management from pre-market approval to on- or post- market surveillance. And the on- or post-market surveillance under the new record-keeping system will certainly be much more stringent.

If you have any other needs or questions, please contact us at service@hfoushi.com.

%22 fill=%22%23fff%22%3E%3Cpath d=%22M.657101983 2.307153C.717756374 2.307153.778028329 2.31550378.836286119 2.33192527L7.50153824 4.21642598C7.78436261 4.29639486 7.97948159 4.5538687 7.97948159 4.84716431V17.3291587c0 .362011299999999-.29419547.6554851-.65712748.6554851C7.26210765 17.9846438 7.20214164 17.9763949 7.14408782 17.9600752L.478835694 16.086013C.195603399 16.0064514.0 15.7486721.0 15.4550964V2.96263815C0 2.60062683.294195467 2.307153.657101983 2.307153zM5.24993201 1.14496912 5.26418414 1.14822796 10.5314278 2.42411481 10.5457819 2.42839204C11.0528159 2.57776403 11.3979008 3.04596771 11.4058555 3.57507096L11.4060595 3.59375837V15.5010512C11.4060595 15.9784967 11.1305779 16.4143157 10.6985524 16.6097188L10.680119 16.6178913 9.23453541 17.2427485C8.92539943 17.3764118 8.56606232 17.2346777 8.43203116 16.9262845 8.30006516 16.6223468 8.43590652 16.2700101 8.73558357 16.1318659L8.74932578 16.1257046 10.1852465 15.504921 10.1853484 15.50431 10.1856544 15.5010512 10.1855524 3.5931728 4.97626062 2.33131424C4.65348442 2.253153 4.45359773 1.93231 4.5239915 1.61039769L4.52728045 1.59616573C4.60567989 1.27415158 4.92725779 1.0747513 5.24993201 1.14496912zM1.2204051 3.70593376V15.0296396l5.53864589 1.5573182V5.2719083L1.2204051 3.70593376zM8.58141076.0158828415 8.59556091.0192689802 13.7740793 1.34834112 13.7845326 1.3513199C14.2915666 1.50079373 14.6366516 1.96902287 14.6446317 2.49810066L14.6447082 2.51678807V14.4240809c0 .477471-.2753541.9132645-.707507100000001 1.108693L13.9188952 15.540921 12.4732861 16.1657782C12.1640737 16.2994415 11.8047365 16.1577075 11.6707819 15.8493142 11.5388159 15.5454019 11.6746572 15.1930398 11.9743343 15.0548956L11.9880765 15.0487343 13.4240227 14.4279507 13.4240992 14.4273652 13.4243031 14.4240809V2.51559147L8.29149858 1.19835809C7.96992068 1.11581778 7.77441926.792301512 7.84909632.471356675L7.85258924.457150168C7.93534844.13630717 8.2596289-.0587140467 8.58141076.0158828415z%22 id=%22ziliao%22/%3E%3C/g%3E%3C/g%3E%3C/svg%3E)

%22/%3E%3C/g%3E%3C/g%3E%3C/svg%3E)

%22%3E%3Cg id=%22%E7%BC%96%E7%BB%84-13%22 transform=%22translate(30.000000, 2950.000000)%22%3E%3Cg id=%22%E7%BC%96%E7%BB%84-3%22 transform=%22translate(15.000000, 950.000000)%22%3E%3Cg id=%22%E7%BC%96%E7%BB%84-27%22 transform=%22translate(40.000000, 215.000000)%22%3E%3Cg id=%22%E7%BC%96%E7%BB%84-10%22 transform=%22translate(0.000000, 144.000000)%22%3E%3Crect id=%22%E7%9F%A9%E5%BD%A2%22 fill=%22%23d8d8d8%22 opacity=%22.01%22 x=%220%22 y=%220%22 width=%2232%22 height=%2232%22/%3E%3Cg id=%22ios-call%22 opacity=%22.4%22 transform=%22translate(4.800000, 4.800000)%22%3E%3Cmask id=%22mask-2%22 fill=%22%23fff%22%3E%3Cuse xlink:href=%22%23path-1%22/%3E%3C/mask%3E%3Cg id=%22Clip-2%22/%3E%3Cpath d=%22M21.739546 17.5430608C20.882919 16.6863974 18.8257249 15.3985249 17.8117151 14.9147941 16.6345314 14.3495128 16.2032859 14.3611681 15.3699694 14.9614517c-.693453.5012501-1.1421814.9673158-1.9406413.7926322C12.631014 15.5850459 11.057587 14.3903428 9.53067187 12.8692553c-1.52676943-1.5267694-2.71564488-3.10019644-2.8846465-3.89865628-.16903805-.80414178.29720975-1.2470426.7924865-1.9406413C8.03875902 6.1966413 8.05627837 5.76539577 7.48516943 4.58821203 7.0014387 3.56837463 5.7193574 1.51704455 4.85690276.660381138 4.00023935-.196245854 3.80789073-.00972487805 3.33596098.159276748c0 0-.69942635.279726829-1.39287935.740001301C1.08641821 1.47049626.608515122 1.94829008.270621138 2.66505366c-.3322120323.7168-.7168 2.0513665 1.241214962 5.53626016C3.09109073 11.0161015 4.64135285 13.1489821 6.94323512 15.4451824L6.95489041 15.4568377c2.30188227 2.3019187 4.42893529 3.8519987 7.24372289 5.4312898 3.4849301 1.9581242 4.8194602 1.573427 5.5362602 1.2413606C20.4516735 21.7972397 20.9295766 21.3193366 21.5006855 20.456882 21.9610693 19.7634289 22.2407961 19.0641119 22.2407961 19.0641119 22.4098341 18.5920364 22.6020371 18.3996878 21.739546 17.5430608z%22 id=%22Fill-1%22 fill=%22%23000%22 mask=%22url(%23mask-2)%22/%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E)

%22%3E%3Cg id=%22%E7%BC%96%E7%BB%84-13%22 transform=%22translate(30.000000, 2950.000000)%22%3E%3Cg id=%22%E7%BC%96%E7%BB%84-3%22 transform=%22translate(15.000000, 950.000000)%22%3E%3Cg id=%22%E7%BC%96%E7%BB%84-27%22 transform=%22translate(40.000000, 215.000000)%22%3E%3Cg id=%22%E7%BC%96%E7%BB%84-10%22 transform=%22translate(0.000000, 206.000000)%22%3E%3Crect id=%22%E7%9F%A9%E5%BD%A2%22 fill=%22%23d8d8d8%22 opacity=%22.01%22 x=%220%22 y=%220%22 width=%2232%22 height=%2232%22/%3E%3Cg id=%22ios-mail%22 opacity=%22.4%22 transform=%22translate(4.800000, 8.000000)%22 fill=%22%23000%22%3E%3Cpath d=%22M22.2035796 1.96720174 16.4132132 8.05344902C16.3701285 8.09790889 16.3701285 8.16447722 16.4132132 8.20893709l4.0521802 4.45365731c.274484099999999.2832104.274484099999999.738603.0 1.0216746C20.3308589 13.8230976 20.1478583 13.8953579 19.9703736 13.8953579 19.7927207 13.8953579 19.6097201 13.8230976 19.4751856 13.684269L15.4391495 9.24730586C15.3961994 9.20298482 15.3261742 9.20298482 15.2830559 9.24730586L14.298364 10.2802603c-.8233514.8607722-1.9158054 1.3382733-3.0889129 1.3438265C10.0201994 11.6296399 8.89004204 11.1132321 8.05592793 10.2413536L7.10877117 9.24730586C7.06568649 9.20298482 6.9957958 9.20298482 6.95271111 9.24730586L2.91667508 13.684269c-.13453454.1388286-.31743424.2110889-.49505346.2110889-.17761922.0-.36051892-.0722602999999999-.49505345-.2110889C1.65211772 13.4011974 1.65211772 12.9458048 1.92656817 12.6625944L5.97878198 8.20893709c.03756877-.044459869999999.03756877-.1110282.0-.155488069999999L.183000601 1.96720174C.112975375 1.89494143.0 1.94498915.0 2.04491106V14.2230629C0 15.2004165.774885285 16.0000347 1.72200841 16.0000347H20.6644372C21.611594 16.0000347 22.3866138 15.2004165 22.3866138 14.2230629V2.04491106C22.3866138 1.94498915 22.2680889 1.90052928 22.2035796 1.96720174z%22 id=%22Fill-1%22/%3E%3Cpath d=%22M11.1933069 10.1747852C11.9897177 10.1747852 12.7376961 9.85266811 13.2973598 9.264L21.7407135.395626898C21.4448721.15132321 21.0788372.00694143167 20.6752336.00694143167H1.71662703c-.40360361.0-.774885288.14438177833-1.065513516.38868546633L9.09446727 9.264C9.64878318 9.84711497 10.3968625 10.1747852 11.1933069 10.1747852z%22 id=%22Fill-2%22/%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E)

%22/%3E%3C/g%3E%3C/g%3E%3C/svg%3E)

%22%3E%3Cg id=%22%E7%BC%96%E7%BB%84-11%22 transform=%22translate(1280.000000, 250.000000)%22%3E%3Crect id=%22%E7%9F%A9%E5%BD%A2%22 stroke=%22%23000%22 fill=%22%23fff%22 x=%22.5%22 y=%22.5%22 width=%2239%22 height=%2239%22 rx=%2219.5%22/%3E%3Cg id=%22%E5%BD%A2%E7%8A%B6%E7%BB%93%E5%90%88-2%22 transform=%22translate(11.500000, 11.500000)%22 fill=%22%23000%22%3E%3Cpath d=%22M1.70710678.292893219 8.424 7.01 15.1421356.292893219C15.5026196-.0675907428 16.0698506-.0953202783 16.4621418.209704612L16.5563492.292893219C16.9468735.683417511 16.9468735 1.31658249 16.5563492 1.70710678L9.839 8.424l6.7173492 6.7181356C16.9468735 15.5326599 16.9468735 16.1658249 16.5563492 16.5563492s-1.0236893.390524299999999-1.4142136.0L8.424 9.839 1.70710678 16.5563492C1.34662282 16.9168331.779391764 16.9445627.387100557 16.6395378L.292893219 16.5563492c-.3905242919-.390524299999999-.3905242919-1.0236893.0-1.4142136L7.01 8.424.292893219 1.70710678c-.3905242919-.39052429-.3905242919-1.023689269.0-1.414213561.390524292-.3905242919 1.023689271-.3905242919 1.414213561.0z%22 id=%22%E5%BD%A2%E7%8A%B6%E7%BB%93%E5%90%88%22/%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E)